The long-anticipated 2020 Summer Olympics will finally take place starting on July 23 in Tokyo. Crowds around the world are slowly building again as the organizers announced that 60,000 fans will be allowed into Wembley Stadium for the Euro Cup finals in July (Source: The Guardian). Foo Fighters, an American rock band, played to a full-capacity audience at Madison Square Garden on June 2. In a sign of what may be to come, attendees had to show proof of vaccination in order to gain entry to the concert.

Strong Investment Returns Tempered with Higher Inflation

The value of the businesses in your mutual fund portfolios generally increased over the quarter. In our view, these higher values are to be greeted with caution because at the same time the values of our investments were increasing the prices we pay for things was also increasing. Year-over-year inflation in Canada was 3.6% in May (up from -0.4% a year earlier) and 5% in the United States (Source: Trading Economics, Statistics Canada, U.S. Bureau of Labour Statistics). The US Federal Reserve, who had previously indicated that they would leave interest rates alone until the end of 2024, now suggest that interest rates will be lifted twice in 2023 (Source: Economist). If our main objective is to maintain and grow purchasing power over time, these inflation numbers remind us that this is not an easy task.

It Pays to be an Owner

Oil prices are up by over 53% since the start of 2021 (Source: Yahoo Canada Finance). It should come as some consolation for you to know that when we invest in Canada through Canadian equity mutual funds, we benefit from these higher prices through ownership of energy businesses such as Enbridge, TransCanada, Canadian Natural Resources and Suncor. Another reminder that ownership is a good thing – and potentially takes some of the pain away when the price of gas creeps up above $1.30/litre.

Bond prices were significantly down over the first quarter and we believe this is important. We were again reminded how fragile our global supply chains are when a ship named MV Ever Given ran aground in the Suez Canal blocked over 12% of global shipments. If it isn’t a pandemic, it’s something else that is reminding us that financial risk is everywhere. We are well-served to understand and manage (versus avoid) risk.

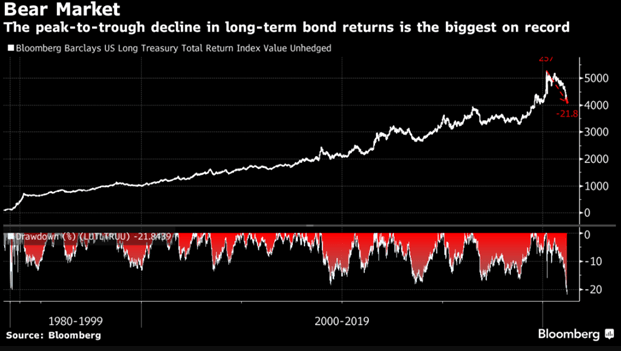

Why Lower Bond Prices is a Big Deal

A decrease in bond-prices is important because bond prices represent the value of money we lend to others. From January 1 – March 31, the iShares Core Canadian Long-Term Bond Index ETF (this serves as a proxy for the value of long-term bonds in Canada) was down 11% (Source: Morningstar).

The graph below shows that interest rates have been more-or-less declining and bond prices have been more-or-less rising since 1981. Since 1981 it has made sense to borrow as much as we possibly could to buy assets that go up in value as the cost of borrowing goes down. The decrease we have seen this year is the first major pullback in bond prices in a generation. How much further bond prices decline and how much higher yields rise is anyone’s guess.

What Do We Do About It?

We want to remain vigilant as the investing landscape changes around us. What causes bond prices to fall and what does it mean? Bond prices often fall when investors require a higher rate of return on the money they lend to others. In many cases they require a higher rate of return when they believe the cost of things will go up. Why, for example, would I lend you my lunch money for 2% this year when I think the price of food will go up by 3% over the same timeframe? Lenders worldwide are expecting prices to rise at a greater rate in the future and have already priced higher interest rates into bond valuations.

What can we do about this? Here are three ideas:

1. Be prepared for declining home values. I am concerned about the number of Canadian households with high mortgages and how they will manage when interest rates increase to 3%, 4% or 5%. I’m interested to know what will happen to the market value of my house when the pool of potential buyers is faced with higher mortgage payments. It is difficult for me to imagine a scenario where housing prices rise in the short to mid-term.

2. Keep our lending short-term. With a bond we receive a promise from borrowers to repay within a specified timeframe. Lending money to others for a longer timeframe in a period of rising inflation is risky. This is because borrowers typically don’t increase what they pay simply because inflation has gone up. With a bond they agree to pay you whatever they agreed to pay you, not a penny more. This is why we prefer to lend our money to others on more of a short-term basis. This strategy is reflected in the portfolios we manage for you.

3. Invest in businesses that have the ability to increase the price of the goods and services they produce. These businesses are able to generate higher profits for investors. This is why we use mutual funds that invest in businesses that are industry leaders and have the ability to thrive while prices are rising.

A Word About ESG Investing

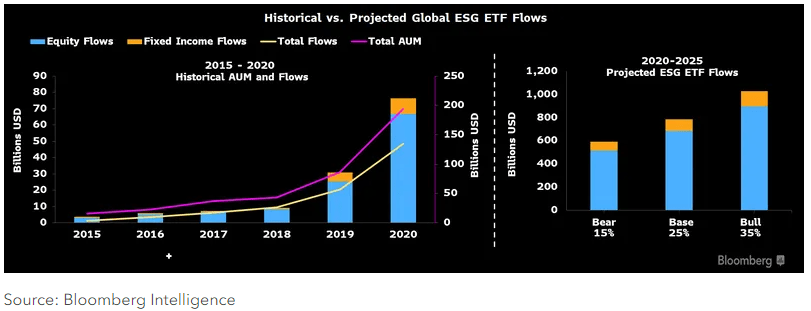

ESG stands for “Environment, Social, Governance” and it is a hot sector in the investing marketplace. The above image shows the explosive growth in ESG assets since 2015. The promise of ESG is that we can use our investment dollars to nudge businesses to be more environmentally aware, socially conscious and better corporate citizens. We have not embraced ESG investing because we believe it is difficult to fulfill the promise that ESG investing makes.

An opinion piece published in USA Today on March 16 by Tariq Fancy, former head of sustainability at BlackRock, the world’s biggest asset manager, tends to support our concern. Click here to read his article.