The Canada Pension Plan (CPP) and Old Age Security (OAS) form the base of Canadian retirement income. If you are entitled to the full CPP and OAS pensions you can receive roughly $23,000/year at age 65 (as of 2022). These programs are not meant to supply your full retirement income and will need to be supplemented by retirement investments or other pension plans.

What is OAS?

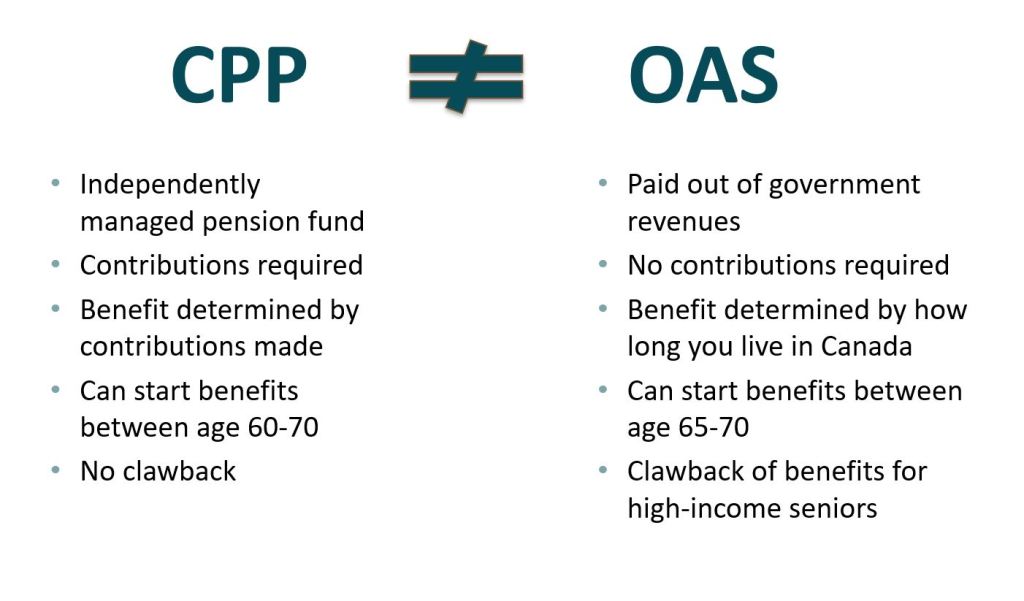

Old Age Security is a monthly payment out of general government revenues. You can begin collecting OAS at any time between age 65 and 70.

Eligibility

If you are living in Canada, you must:

- Be 65 years old or older

- Be a Canadian citizen or legal resident at time of OAS approval

- Have resided in Canada for at least 10 years since the age of 18

If you are living outside Canada, you must:

- Be 65 years old or older

- Have been a Canadian citizen or legal resident of Canada on the day before you left Canada

- Have resided in Canada for at least 20 years since the age of 18

To receive full OAS benefits you need to have lived in Canada at least 40 years after age 18.

How much can you collect?

The 2022 payment is $666.83/month (8,004/year) if you began collecting at 65 and are eligible for the full amount. If you are 75 and over, an automatic 10% increase to your OAS was enacted July 2022.

For every month you delay OAS the benefit payment increases by 0.6% (7.2%/year) up to a maximum increase of 36% at age 70. If you delay benefits till age 70 the monthly benefit is $906.89 ($10,883/year).

Guaranteed Income Supplement (GIS)

GIS is an additional tax-free monthly payment for low-income seniors. Low-income in 2022 is considered below $20,208 if single or $26,688 as a couple (not including OAS/GIS income). The amount of benefit received depends on the net income of the previous tax year. To calculate your exact eligibility refer to the Government of Canada website.

OAS pension recovery Tax (clawback)

OAS clawback refers to the repayment of OAS benefits at net income levels over $81,761 (2022). For every dollar of net income above this threshold 15 cents of OAS is repaid. OAS is fully repaid at $134,253 (under age 75) or $136,920 (age 75 and over). Effectively this is a 15% additional tax on income between these thresholds, resulting in some of the highest marginal tax rates in Canada.

What is CPP?

Canada Pension Plan (CPP) is a contributory pension plan. All employees and self-employed individuals in Canada (except Quebec, which has QPP) contribute to CPP. These individuals then receive pension income in retirement.

Contributions

Employees contribute 5.70% of employment income with the employer matching the contribution. The maximum contribution for an employee is $3,499.80 (2022) and there are no contributions on employment income over $64,900 (2022). A self-employed individual must pay both the employee and employer portions; therefore, the rate is 11.40% to a maximum of $6,999.60 in 2022.

Investment Fund

Unlike OAS, the Canada Pension Plan is an independently managed pension fund. It is separate from government revenues/expenses and is managed by an arm’s length organization, CPP Investments. The mandate of CPP Investments is “to invest the assets of the CPP Fund with a view to achieving a maximum rate of return without undue risk of loss.”

As of March 31, 2022, the fund value was $539 billion, and the fund had a rate of return of 10.8%/year over the last 10 years. The investments within the fund are wide-ranging, from Canadian farmland to publicly traded companies and private equity.

The CPP Investment Fund is subject to actuarial review every 3 years by the Office of the Chief Actuary. This is a fully independent office that reviews various pension plans and social programs, including CPP and OAS, to ensure that they are stable, secure and being managed appropriately. The most recent report on CPP was issued December 2019 where it was noted that CPP is sustainable for at least the next 75 years.

How much can you collect?

The CPP benefits you collect in retirement are determined by three main factors:

- Amount contributed annually

- Number of years contributions were made

- Age that pension withdrawals begin

To receive maximum CPP you need to have contributed the maximum amount for 39 years between 18 and 65. You can refer to your My Service Canada Account for your CPP estimate.

The maximum monthly amount you could receive if you started your pension at 65 is $1,253.59 (2022). Meanwhile the average benefit is $727.61/month in 2022.

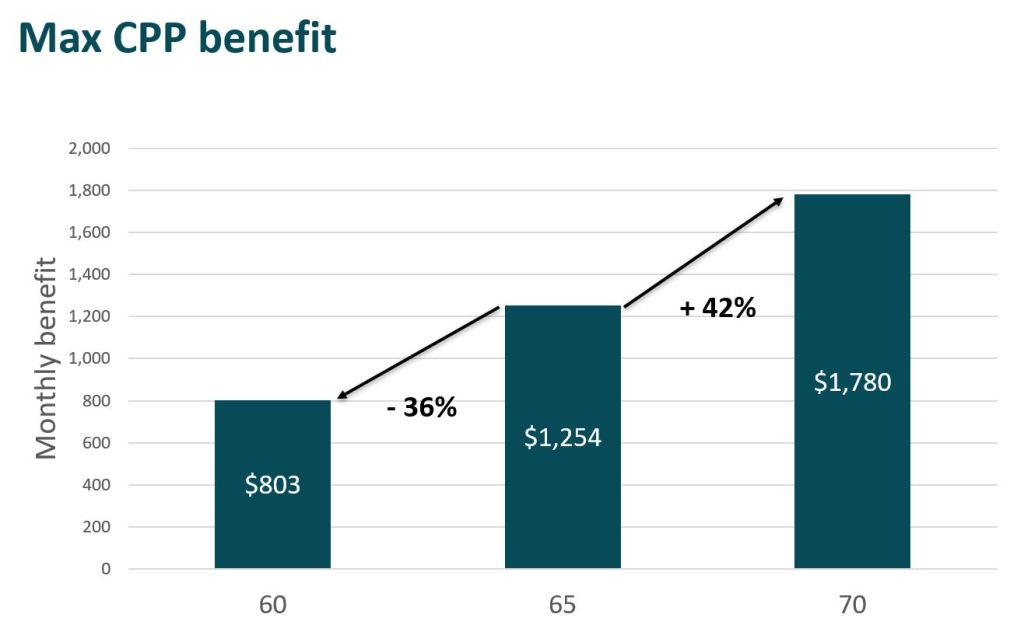

CPP benefits can be started at any time between age 60 and 70. For every month before your 65th birthday that you begin CPP benefits your pension is reduced by 0.6% (7.2%/year) for a maximum reduction of 36% if taken at age 60. Each month you delay CPP after your 65th birthday increases your pension by 0.7% (8.4%/year) for a maximum increase of 42% if started at age 70.

Therefore, if you were eligible for maximum CPP your monthly payment could be between $803 (age 60) and $1,780 (age 70) depending on when you begin withdrawing your benefits.

Refer to the CPP website for further details such as post-retirement benefit, disability pension, survivor’s pension and more.

Differences

Although Canada Pension Plan and Old Age Security are pensions to support Canadian retirees, they have significant differences.

In our next post we will explore the benefits of delaying your pensions.