In our August 2022 blog post we reviewed the details of CPP and OAS. Now we can address one of the most frequent questions we hear from pre-retirees:

When should I start taking CPP and OAS?

This is an important question for those approaching retirement and the decision can dramatically change the chance of running out of money in late retirement.

Impact of Start Date on Benefits

Old Age Security – Benefits can begin anytime between ages 65 and 70

- For every month after age 65 that you start your benefits, your monthly payment is increased by 0.6% (7.2%/year). Maximum increase of 36% if started at age 70.

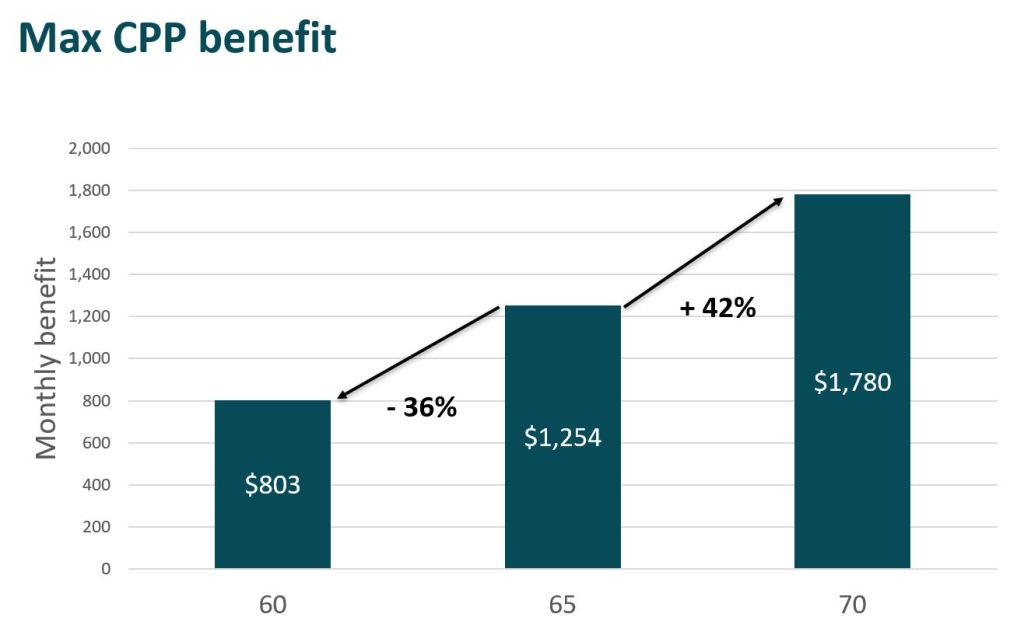

Canada Pension Plan – Benefits can begin anytime between ages 60 and 70

- For every month before age 65 that you start your benefits, your monthly payment is reduced by 0.6% (7.2%/year). Maximum reduction of 36% if started at age 60.

- For every month after age 65 that you start your benefits, your monthly payment is increased by 0.7% (8.4%/year). Maximum increase of 42% if started at age 70.

The benefits of delaying CPP & OAS are significant, yet most Canadians do not take advantage. In fact, the 2020 paper Get the Most from the Canada & Quebec Pension Plans by Delaying Benefits noted that:

- Over 95% of Canadians have consistently taken CPP at age 65 or earlier. Less than 1% of Canadians delay till age 70. Historically the most popular age to take CPP is age 60.

The author also calculated that:

- An average Canadian receiving the median CPP income who takes their benefits at age 60 rather than age 70 is giving up over $100,000 (in today’s dollars) worth of secure lifetime income.

- By delaying CPP from age 60 to age 70 the average Canadian will receive over 50% more CPP income over the course of their retirement.

The results are similar with OAS. Most Canadians begin taking OAS as soon as they turn 65 and therefore give up a significant amount of lifetime income.

Why Don’t Canadians Delay Their Benefits?

There are many reasons that Canadians choose not to delay their CPP and OAS benefits, including:

Lack of advice – a 2018 Government of Canada poll found that more than two thirds of Canadians nearing or in retirement do not understand that waiting to take their CPP benefits will increase their monthly pension payments. (Employment and Social Development Canada, 2020)

Bad advice – much of the financial planning advice focuses on the “breakeven age” which is the age you need to live till to receive more money by delaying.

- This approach is misleading and doesn’t consider the largest risk for most retirees – the risk of outliving their savings (longevity risk).

Stability of CPP and OAS pensions – Canadians are concerned these pensions will not be around in the future

- CPP is one of the most stable pension plans in the world. Significant changes were made in the 1990s to the structure and funding to ensure stability. The most recent report on CPP (completed by the Office of the Chief Actuary) said the pension is sustainable for at least the next 75 years.

- OAS comes from general government revenues, so it is more vulnerable to cutting by the Canadian government. Yet seniors are one of the most important voting blocks in elections and reducing OAS benefits would be politically disastrous.

Fear and uncertainty – no one knows how long they will live so many opt to think in the short term and secure the money now rather than consider the long-term impact.

- The greater risk to most retirees is that they outlive their savings. The average life expectancy of a 60-year-old in Canada is now 86 years old. This means retirement savings need to last 20-30 years. Delaying CPP and OAS locks in a much higher secure income, thereby reducing the chance of outliving your money.

General Recommendations

- Delay the start of CPP and OAS while fully employed.

- It is more beneficial to delay CPP after age 65 than OAS.

- Delaying CPP – increases benefits by 0.7% per month after age 65

- Delaying OAS – increases benefits by 0.6% per month after age 65

- High-income seniors should seriously consider delaying OAS due to the OAS clawback.

- For every dollar of taxable income above the threshold ($81,761 in 2022) you must repay $0.15 of OAS income. By delaying OAS, you can avoid the 15% OAS clawback until age 70.

Conclusion

Most Canadians in reasonable health who can afford to delay their CPP and OAS benefits should do so. The biggest risk for retirees is not having secure income for life and delaying pension benefits can help address this risk.

We encourage you to seek advice from an expert on your personal situation as the decision should be considered within the broader context of your retirement plan. Each situation is unique and deserves specific contemplation. We would be happy to help you if you have any questions or need help analysing this decision.

Citations

MacDonald, B.J., (2020). Get the Most from the Canada & Quebec Pension Plans by Delaying Benefits: The Substantial (and Unrecognized) Value of Waiting to Claim CPP/QPP Benefits. National Institute on Ageing, Ryerson University.

Employment and Social Development Canada (ESDC) (2020). Summary – ESDC Survey on Pension Deferral Awareness. Ottawa, ON: Government of Canada.

Office of the Chief Actuary. (2019). 30th Actuarial Report on the Canada Pension Plan as at 31 December 2018. Office of the Superintendent of Financial Institutions.