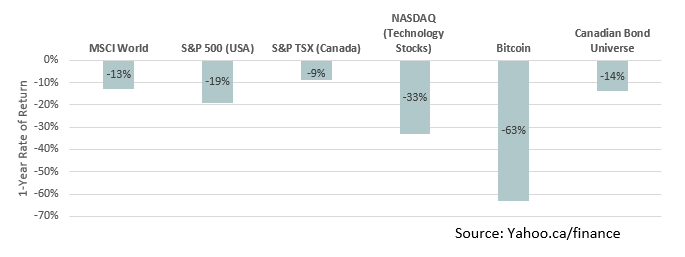

A new year with new investment realities to consider. The year 2022 brought headwinds in the form of ongoing COVID-related challenges especially in China, wildly fluctuating energy prices, skyrocketing inflation, the ongoing war in Ukraine and increasing interest rates that reversed a trend that dates back 40 years. The value investors placed on securities decreased over the course of the year 2022 as follows:

Our observations

- Canadian businesses. Our thesis for years has been that Canadian businesses – many of which are in the energy and materials sectors – serve as a healthy part of a diversified global portfolio. This year portfolios with a Canadian equity component benefitted greatly.

- Bonds. Which have long been considered a safe-haven for investors, experienced one of the most pronounced selloffs in modern history with the Canadian Bond Index declining by 14% over the course of the year.

- Active management. Many active managers were able to substantially outperform their peers and passive investments over the course of the year. While this is small consolation for investors whose values went down in 2022, the capital protection provided by active management served many investors well in 2022.

- Crypto-currency. Speculators in crypto-currency saw the value of their portfolios drop by 60% or more in 2022. FTX Trading Limited, a large crypto-currency exchange, declared Chapter 11 bankruptcy in the US and one of its founders, is facing charges that could keep him imprisoned for the rest of his life. The events of 2022 in this space serve as a cautionary tale on the perils of speculation of any kind.

Looking Ahead in 2023

Looking ahead, we are wise to consider the following:

- Inflation and tax. Our goal is to invest in a manner that enables you to feed, clothe and house you and your family in the future. The greatest threat to achieving this goal is not short-term volatility but inflation and tax. Together we will continue pursue a strategy that enables you to manage and overcome these threats over the long term.

- Investing in businesses. While income-generating investments such as High Interest Savings Accounts and GICs are generating much higher rates of return, they do not enable your purchasing power to keep pace with the cost of inflation and tax. Our investment priorities remain unchanged: we believe that a diversified mutual fund portfolio made up of quality businesses acquired at reasonable prices will enable your long-term financial success. Many businesses can adapt and thrive in an inflationary world. Think of it this way, when the price of doughnuts goes up would you rather be the one paying for the doughnuts or being an owner of the restaurant that serves the doughnuts?

- There are benefits associated with higher inflation as follows:

- Tax brackets announced for 2023 are substantially higher than 2022. This means that your taxes will be lower on the same income level. The OAS claw back threshold has also increased substantially for 2023.

- OAS and CPP Retirement benefits have increased substantially for 2023.

- Tax-Free First Home Savings Account (FHSA). The federal government will launch the FHSA this year. While this account may not benefit you, it is likely that a family member or friend could benefit. We will keep you posted on this as we learn more and as the account is launched later in 2023.