We are continuing with the theme of debt repayment. Last month we reviewed how to choose between debt repayment and investing. This month we’ll explore two different debt repayment methods: the snowball method, and the avalanche method.

Snowball Method

The snowball method approaches debt repayment from a psychological and human nature basis by providing positive reinforcement. You repay the smallest debt balance first while making minimum payments on the rest. Then once you have repaid the first debt you tackle the next smallest debt and so on. You do not consider the interest rate of the individual debts. The snowball method focuses on providing wins and positive reinforcement as individual debts are paid off.

Avalanche Method

The avalanche method approaches debt repayment from an efficiency basis. You repay the debt with the highest interest rate first while making minimum payments on the rest. Once that debt is repaid you focus on the next highest interest rate debt. This method aims to minimize your interest costs and get you out of debt as quickly as possible.

Example

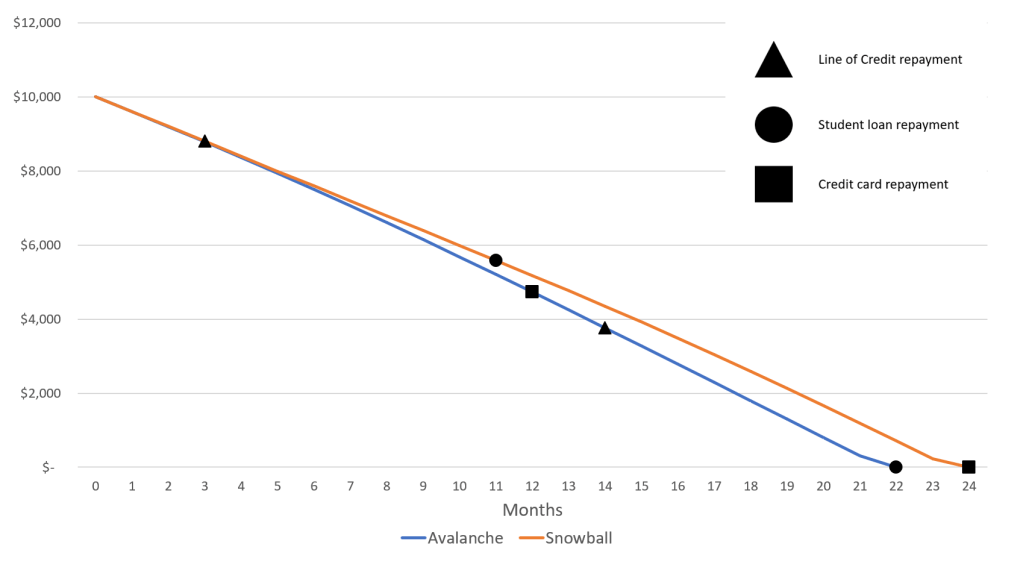

You have an extra $500/month you can use to repay debt (after minimum payments). You have the following debts:

- $4,000 student loan debt at 3.50%

- $1,000 line of credit debt at 7.00%

- $5,000 credit card debt at 19.99%

Using the avalanche method the debt is paid off in 22 months and total interest paid is $805.15. Under the snowball method the debt is paid off in 24 months and total interest paid is $1,729.37.

The avalanche method results in less interest and a quicker payoff period. The downside is that it takes about a year to pay off the first debt which may cause you to lose motivation and miss payments. The loss of motivation is even more likely when the debt balances are larger and the payoff periods much longer than what is shown in this example.

Under the snowball method you pay off the line of credit in just over two months and pay off the student loan in under a year. Paying these off provides positive reinforcement and keeps you motivated to repay the remaining debt.

Conclusion

Choosing between the two methods comes down to knowing who you are as a person and what motivates you. Honestly assess yourself. Will seeing individual debts being eliminated motivate you to stay on the journey? Or will knowing you are using the most efficient method be enough motivation for you?

Although we are partial to the most efficient debt repayment option (avalanche), the goal is to continually make progress paying off the debt and putting yourself in a better financial position. Having a good plan that you can stick to is more important than having the perfect plan.