Admittedly, not the most interesting title. You likely have never heard the phrase “sequence of returns risk” but I guarantee that those of you approaching retirement have thought about it.

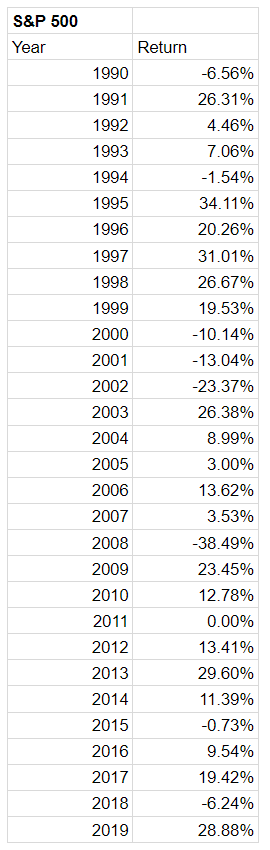

Sequence of returns risk comes from the order in which your investment returns occur. Your investments will earn a return each year and these returns fluctuate (see the returns for the S&P 500 for the 30 years from 1990 to 2019). Even though the average return over that period was 9.11% it fluctuated from +34.11% to -38.49%.

BUT Does it matter which order the returns come in?

I have reordered the 30-year annual returns into a bad start order and a good start order to examine the impact. The average over the 30 years is still 9.11% using either order.

Let’s examine the impact of the order of returns in different investment scenarios.

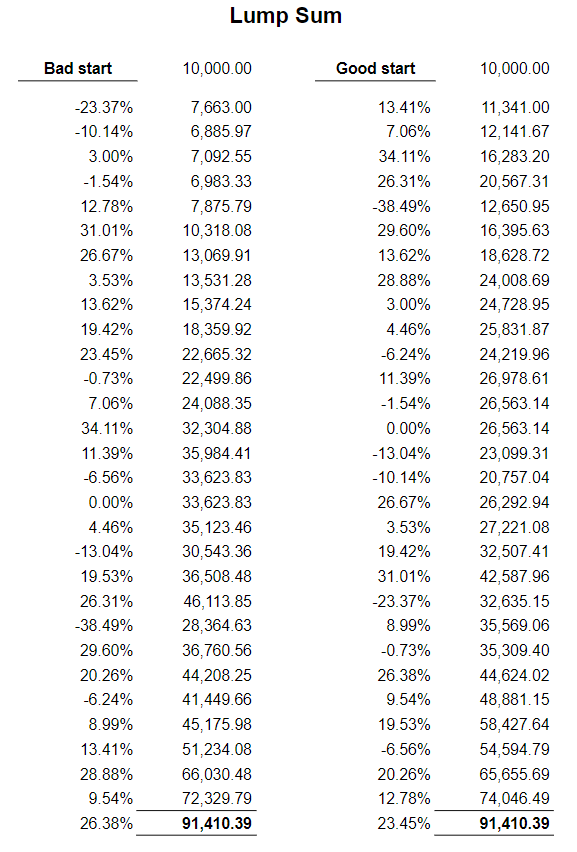

Lump sum investment

Both scenarios start with a lump sum investment of $10,000. After the first 4 years there is almost three times more money with the good start. Yet, both end up in the same place after 30 years. The order of the returns does not matter if there are no contributions or withdrawals.

Annual investment returns source: S&P 500

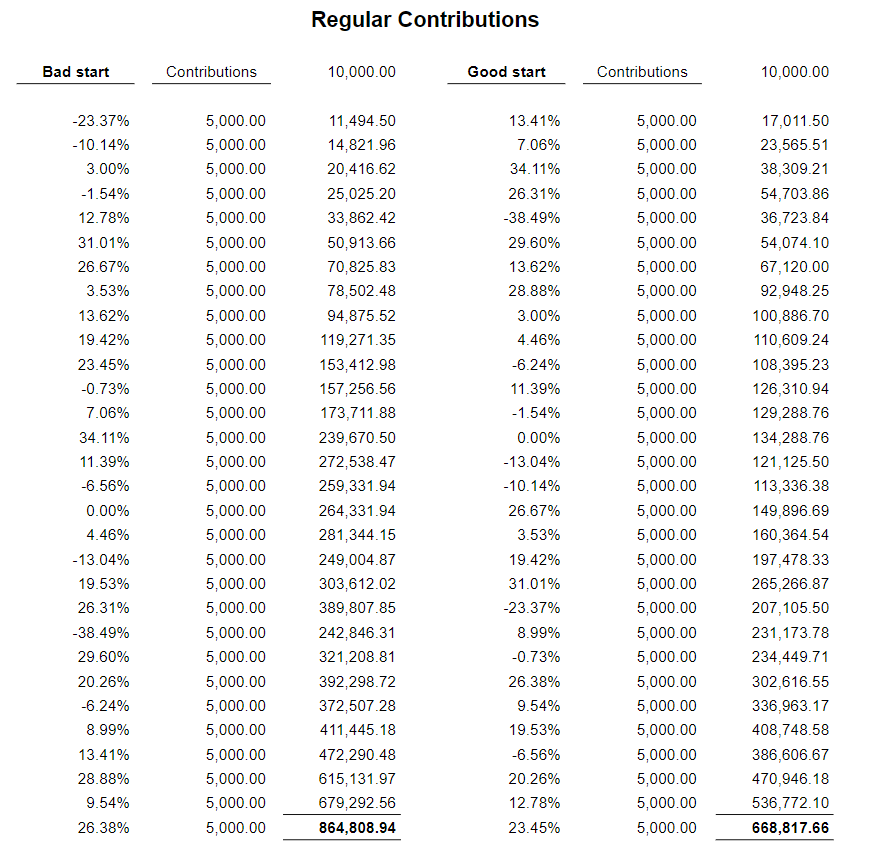

Lump Sum Investment With Regular Contributions

Again, we start with $10,000, but now each year another $5,000 is added. You might expect that a bad start to investment returns would be terrible. In fact, a bad start is better! (As long as the average return is the same).

Under the bad start there is about $865,000 at the end of 30 years while the good start has only $669,000. With the same average return, you would have 29% more money at the end of 30 years if you had a bad start to your investment journey (and a good finish).

Annual investment returns source: S&P 500

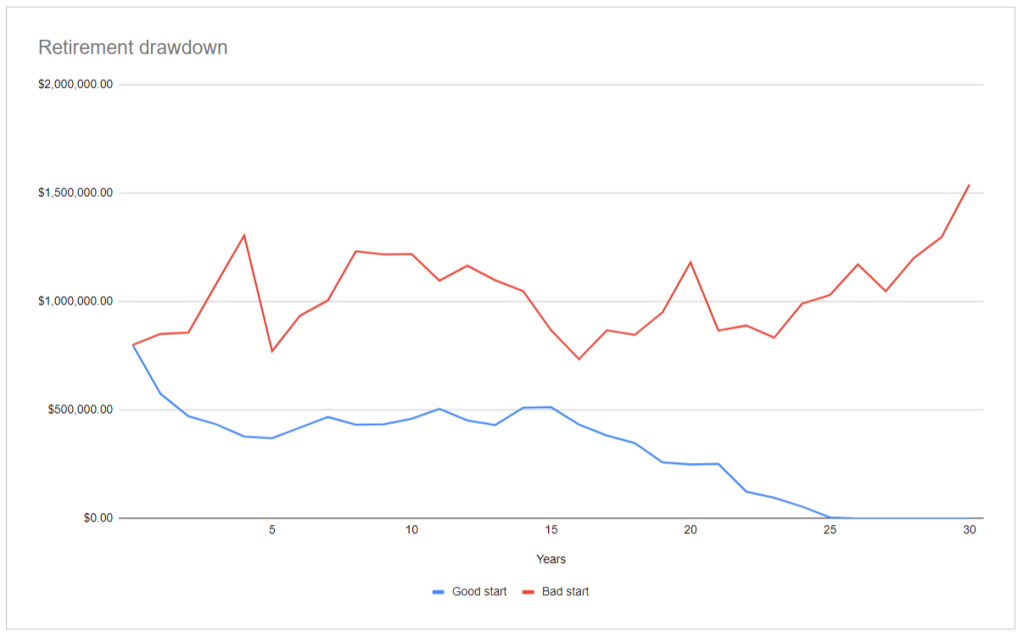

Retirement Drawdown

This is the classic scenario when sequence of returns risk is discussed. You have reached retirement with $800,000 and plan to withdraw $50,000 every year for the next thirty years.

If you happen to retire right before a string of bad investment years your retirement can be severely affected. With the bad start order you run out of money before the end of year 26. Under the good start order you would have $1,539,000 left at the end of the 30 years. This is a massive difference considering the average return is the same.

Created by Thomson Allison Financial Solutions

What are some solutions?

If you have saved for decades, the last thing you want to hear is that a string of bad years to start your retirement could derail the whole thing. So, what are some strategies to deal with this risk?

There is nothing we can do as investors to change the behaviour of financial markets, but we can mitigate the impacts of sequence of returns risk. Here are two strategies:

1. Flexible Withdrawal Strategy

In years where the market is down you cut spending and reduce withdrawals. This reduces the impact of a down market as more funds are available for the future increases. This strategy has some limitations as spending tends to be difficult to cut.

When markets recover spending can be increased again. The flexibility allows you to weather the storms during retirement.

2. Cushion Strategy

This is a strategy we employ for our clients. Separate the investments into different time periods based on when you expect to spend the money.

- Short-term (1 – 2 years) is invested in a cash equivalent such as a high-interest savings account.

- Medium-term (3 – 5 years) is invested in fixed income funds (bonds)

- Long-term (5+ years) is invested in equity funds (stocks)

The investor’s situation and risk tolerance are an important consideration when applying this strategy.

We refer to the short- and medium-term investment periods as your “cushion” investments. If there is poor stock market performance, you can draw money from the cushion until those investments recover. This avoids withdrawing from assets that are down in value.

Conclusion

Sequence of returns is a legitimate risk when entering retirement and your portfolio should be adjusted to protect your investments. A string of bad investment years as you begin retirement can derail your plan if you are not properly prepared.

The above strategies limit your need to make withdrawals from equity investments during a downturn in the market, protecting your long-term retirement health.