One of the first questions when Canadians begin saving and investing is:

What account do I use, the RRSP or the TFSA?

The RRSP has a long history and Canadians have used it for their retirement investing for decades. Meanwhile the TFSA is the new(er) kid on the block and is quickly gaining in popularity. While the choice between RRSP and TFSA comes down to your particular situation there are some general principles that can inform your decision.

A brief description of each account:

The RRSP (Registered Retirement Savings Plan) is intended for retirement savings. Any contributions made to the plan are deducted from your taxable income. The growth and earnings accumulate tax-free. Withdrawals are considered income and are taxable.

The TFSA (Tax Free Savings Account) is intended to be more flexible and used for other savings goals in addition to retirement. The contributions are not deducted from taxable income and withdrawals are not considered income and therefore not taxable. As with the RRSP, the growth and earnings within the plan accumulate tax-free.

Both of these accounts can hold the same types of investments including stocks, bonds, mutual funds, ETFs and more.

General guidance on your choice

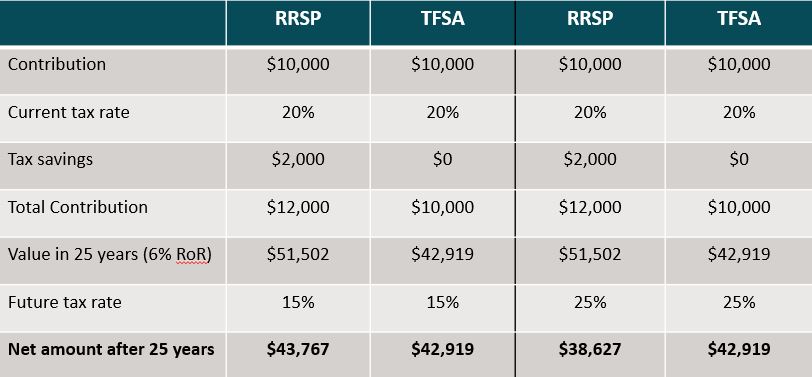

The general guidance on when to use each account is based around your current and future tax brackets. If you are paying taxes in a higher bracket when contributing than when withdrawing the RRSP makes the most sense. If your tax bracket will be the same or higher when you withdraw the money then the TFSA makes more sense. Here is a quick example:

In the first comparison, there is more money after-tax when using the RRSP. This is due to the lower tax rate when the funds were withdrawn. In the second comparison you would have more after-tax money available if you had saved within the TFSA. The tax rates don’t affect the results of investing in the TFSA but they have a large impact on the RRSP results.

Keep in mind the benefit of the RRSP is dependent on contributing more than you would in the TFSA (the tax deduction allows you to contribute more to the RRSP).

Additional RRSP features:

The Home Buyers’ Plan allows RRSP account holders to withdraw up to $35,000 for a home down payment without paying immediate taxes. Keep in mind this is only available if you are considered a first-time home buyer purchasing a qualifying home. More information and rules about the HBP can be found here.

You are allowed to withdraw the money out under the HBP without paying taxes but you must repay the funds over a 15 year period starting the second year after the year you withdraw the funds. If you don’t make the repayments, 1/15th of the amount withdrawn will be added to your income each year starting at the first required repayment year.

There is a similar plan called the Lifelong Learning Plan that allows you to withdraw up to $20,000 ($10,000 per year) to fund the pursuit of your education and repay it over a 10 year period. More information can be found here.

Flexibility of the TFSA

The TFSA is a much more flexible savings vehicle as it allows you to withdraw funds without worrying about the tax consequences. This can be great for emergencies, large purchases and in your retirement. Since TFSA withdrawals are not considered income they also do not affect eligibility for federal income-tested benefits and credits, such as GIS and OAS clawback.

Withdrawals from the TFSA are added back onto the contribution room the next year. This is not the case with the RRSP as withdrawals do not affect contribution room. This allows you to withdraw money from the TFSA and then reinvest that same amount back into the TFSA in the future.

Conclusion

The TFSA should be the first stop savings vehicle for investors unless they are in a high tax bracket now and expect to be in a lower one when the funds are withdrawn. The flexibility of the TFSA and ability to withdraw without worrying about taxes makes it a more useful vehicle.

On the other hand, if you have trouble leaving your savings alone, maybe the tax payment on RRSP withdrawals will stop you from withdrawing and spending your savings.

If you have questions about your specific situation please send us an email or give us a call.