On April 1, 2023 a new registered account will join the RRSP and TFSA. The Tax-free First Home Savings Account (FHSA) is being introduced to help first-time home buyers save for a down payment.

How does it work?

The FHSA combines elements of the TFSA and RRSP. Similar to an RRSP your contributions are tax deductible. Meanwhile your withdrawals, if used to buy a home, are tax-free like withdrawals from a TFSA. Investment income earned in the plan is also tax-free. These features combine to form an incredibly attractive vehicle to accumulate a home down payment.

Who can open a FHSA?

To open a FHSA you must be:

- A Canadian resident

- At least 18 years of age and not over 71 years of age

- First-time home buyer, meaning you haven’t owned a home in which you lived at any time during the year of account opening or the preceding four calendar years

Contribution limits and rules

- You are allowed to contribute a total of $8,000 annually, up to a maximum lifetime contribution amount of $40,000

- Overcontributions are taxed at 1% per month

- You must open a plan to start accumulating contribution room

- Unused contribution room can be carried forward. For example, if you contribute $5,000 in 2023 you could contribute up to $11,000 in 2024 ($8,000 – $5,000 + $8,000)

- The unused contributions you can use in a year is limited to $8,000, therefore the most you can contribute in any one year is $16,000, the $8,000 unused contribution carry forward and $8,000 current year contribution

- Unlike an RRSP, contributions made within the first 60 days of a calendar year cannot be claimed in the prior year

- The FHSA deduction does not have to be used in the same tax year as the contribution and can be carried forward to a future year

Withdrawal Rules

For an FHSA withdrawal to be a qualifying withdrawal, you must:

- Be a first-time home buyer at the time a withdrawal is made. There is an exception that allows you to make a qualifying withdrawal within 30 days of moving into the home

- You must have a written agreement to buy or build a qualifying home before October 1 of the year following the year of withdrawal and intend to occupy the home as your principal residence within one year after buying or building it

- A qualifying home would be a housing unit located in Canada

- A housing share that only provides the right to tenancy in the housing unit would not qualify

If these conditions are met the entire FHSA can be withdrawn on a tax-free basis.

What if i don’t buy a house?

The FHSA can be kept open for 15 years. If at the end of the 15 years you have not purchased a home the following options are available:

- Take non-qualifying withdrawal – the withdrawal would be treated as taxable income

- Transfer to an RRSP or RRIF – the transfer would happen without an immediate tax impact and would be treated the same as all the other funds in the RRSP/RRIF going forward.

- The transfer would not reduce or be limited by your available RRSP contribution room.

Treatment on Death

Similar to a TFSA you are able to designate your spouse or common-law partner as the successor account holder. This allows your successor holder to become the new holder of the FHSA upon your death. If the surviving spouse is not eligible to open an FHSA the amount could be transferred to an RRSP/RRIF or withdrawn as taxable income.

If the beneficiary of the FHSA is not the spouse or common-law partner, the funds would need to be withdrawn and would be taxable income of the beneficiary.

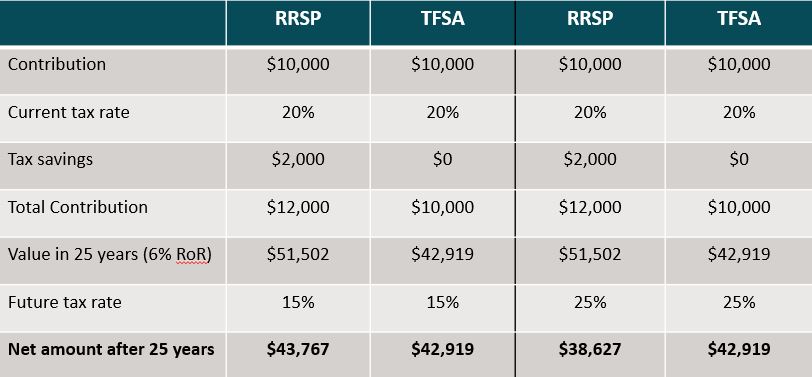

Saving for a home – TFSA vs. RRSP vs. FHSA

| TFSA | RRSP | FHSA | |

| Annual contributions | $6,666.67 | $6,666.67 | $6,666.67 |

| Tax savings (20% rate) | $0 | $1,333.33 | $1,333.33 |

| Total annual contributions | $6,666.67 | $8,000.00 | $8,000.00 |

| Total contributions (5 years) | $33,333.35 | $40,000.00 | $40,000.00 |

| Value after 10 years (5% return) | $47,015 | $56,418 | $56,418 |

| Taxes on withdrawal (20% rate) | $0 | $4,284* | $0 |

| Net withdrawal | $47,015 | $52,134 | $56,418 |

- *Home Buyers Plan has a maximum tax-free withdrawal of $35,000. The remaining $21,418 would be taxable income. The Home Buyers Plan (HBP) withdrawals must also be repaid over 15 years.

Other considerations

You can make both a FHSA withdrawal and a HBP withdrawal from your RRSP on the same home purchase. This gives access to the $35,000 of HBP withdrawals plus the balance of your FHSA as tax-free withdrawals for a home purchase.

You can transfer funds from your RRSP to your FHSA to take advantage of the tax-free withdrawal for home purchase. The transfer from your RRSP to FHSA is limited by the FHSA annual and total contribution limit. Therefore, this would only make sense in specific instances.

Conclusion

The FHSA is a better account than both a TFSA and RRSP for saving for a home. The tax-free withdrawals and lack of repayment makes it a better choice than an RRSP. While the tax deductibility of contributions makes it preferrable to a TFSA.

Even if you are not sure if you will buy a home, it should be used for retirement savings before an RRSP because the FHSA balance can be moved to an RRSP tax-free. This gives you an added $40,000 in lifetime RRSP contribution room.

Anyone who qualifies to open an FHSA should do so and deposit at least a nominal amount to begin accumulating contribution room. If you will be purchasing a home in the coming years you should be using the FHSA to save for the down payment.