Spring is in the air, stock markets are up and, as always, we face an uncertain future. This morning I am reviewing our quarterly newsletters written before the pandemic and hoping you will join me as I reflect with you not on the past three months but the past three plus years.

IF We’d Known Back THen What We KNow NOw…

In the January 2020 edition of this newsletter I invoked Mike Tyson’s famous quote: “Everybody has a plan until they get punched in the face”. We investors have since been “punched in the face” many times. Consider that we:

were hit by a global pandemic

took on ballooning government deficits

looked on in shock as a war started in Europe

found ourselves in an inflationary environment not seen in 30 years

endured sharp interest rate increases while the value of our homes declined

witnessed bank failures including the 40-year-old Silicon Valley Bank and 167-year-old Credit Suisse

…and this list is far from complete. All this makes me wonder:

If we had known back then what we know now about the first three years of the decade, would we have kept our money invested in businesses or would we have moved to so-called “safe” investments?

The Results are In

In January 2020 I encouraged you to “look forward with planning in mind – and continue to be prepared for the uncertainty we face”. Weeks later we entered the pandemic. We were nervous for our health, for our communities and for our investments. You were steadfast and stuck to the plan. The results are in over three years later:

Sticking to the Plan: A $100,000 investment in the S&P/TSX Index (the 250 largest Canadian businesses) made on January 1, 2020 would have been worth over $131,900 by March 31, 2023 (Source: Morningstar. Compound Annual Growth: 8.9%).

Not sticking to the Plan: If you had invested in GICs over the same timeframe your $100,000 investment would have grown to $108,356 (Source: Ratehub.ca. Compound Annual Growth: 2.5%).

That’s a 23.5% difference in just over 3 years.

Are THings Looking Up for First-Time Homebuyers?

For many young Canadians, we see an opportunity to acquire homes at prices lower than they have been for some time owing to higher interest rates. We will also be recommending that many of our clients (or their younger family members/friends) set up Tax Free First Home Savings Accounts. For more information on this account I recommend you check out our blog post.

A new year with new investment realities to consider. The year 2022 brought headwinds in the form of ongoing COVID-related challenges especially in China, wildly fluctuating energy prices, skyrocketing inflation, the ongoing war in Ukraine and increasing interest rates that reversed a trend that dates back 40 years. The value investors placed on securities decreased over the course of the year 2022 as follows:

Our observations

Canadian businesses. Our thesis for years has been that Canadian businesses – many of which are in the energy and materials sectors – serve as a healthy part of a diversified global portfolio. This year portfolios with a Canadian equity component benefitted greatly.

Bonds. Which have long been considered a safe-haven for investors, experienced one of the most pronounced selloffs in modern history with the Canadian Bond Index declining by 14% over the course of the year.

Active management. Many active managers were able to substantially outperform their peers and passive investments over the course of the year. While this is small consolation for investors whose values went down in 2022, the capital protection provided by active management served many investors well in 2022.

Crypto-currency. Speculators in crypto-currency saw the value of their portfolios drop by 60% or more in 2022. FTX Trading Limited, a large crypto-currency exchange, declared Chapter 11 bankruptcy in the US and one of its founders, is facing charges that could keep him imprisoned for the rest of his life. The events of 2022 in this space serve as a cautionary tale on the perils of speculation of any kind.

Looking Ahead in 2023

Looking ahead, we are wise to consider the following:

Inflation and tax. Our goal is to invest in a manner that enables you to feed, clothe and house you and your family in the future. The greatest threat to achieving this goal is not short-term volatility but inflation and tax. Together we will continue pursue a strategy that enables you to manage and overcome these threats over the long term.

Investing in businesses. While income-generating investments such as High Interest Savings Accounts and GICs are generating much higher rates of return, they do not enable your purchasing power to keep pace with the cost of inflation and tax. Our investment priorities remain unchanged: we believe that a diversified mutual fund portfolio made up of quality businesses acquired at reasonable prices will enable your long-term financial success. Many businesses can adapt and thrive in an inflationary world. Think of it this way, when the price of doughnuts goes up would you rather be the one paying for the doughnuts or being an owner of the restaurant that serves the doughnuts?

There are benefits associated with higher inflation as follows:

Tax brackets announced for 2023 are substantially higher than 2022. This means that your taxes will be lower on the same income level. The OAS claw back threshold has also increased substantially for 2023.

Tax-Free First Home Savings Account (FHSA). The federal government will launch the FHSA this year. While this account may not benefit you, it is likely that a family member or friend could benefit. We will keep you posted on this as we learn more and as the account is launched later in 2023.

In our August 2022 blog post we reviewed the details of CPP and OAS. Now we can address one of the most frequent questions we hear from pre-retirees:

When should I start taking CPP and OAS?

This is an important question for those approaching retirement and the decision can dramatically change the chance of running out of money in late retirement.

Impact of Start Date on Benefits

Old Age Security – Benefits can begin anytime between ages 65 and 70

For every month after age 65 that you start your benefits, your monthly payment is increased by 0.6% (7.2%/year). Maximum increase of 36% if started at age 70.

Canada Pension Plan – Benefits can begin anytime between ages 60 and 70

For every month before age 65 that you start your benefits, your monthly payment is reduced by 0.6% (7.2%/year). Maximum reduction of 36% if started at age 60.

For every month after age 65 that you start your benefits, your monthly payment is increased by 0.7% (8.4%/year). Maximum increase of 42% if started at age 70.

The benefits of delaying CPP & OAS are significant, yet most Canadians do not take advantage. In fact, the 2020 paper Get the Most from the Canada & Quebec Pension Plans by Delaying Benefits noted that:

Over 95% of Canadians have consistently taken CPP at age 65 or earlier. Less than 1% of Canadians delay till age 70. Historically the most popular age to take CPP is age 60.

The author also calculated that:

An average Canadian receiving the median CPP income who takes their benefits at age 60 rather than age 70 is giving up over $100,000 (in today’s dollars) worth of secure lifetime income.

By delaying CPP from age 60 to age 70 the average Canadian will receive over 50% more CPP income over the course of their retirement.

The results are similar with OAS. Most Canadians begin taking OAS as soon as they turn 65 and therefore give up a significant amount of lifetime income.

Why Don’t Canadians Delay Their Benefits?

There are many reasons that Canadians choose not to delay their CPP and OAS benefits, including:

Lack of advice – a 2018 Government of Canada poll found that more than two thirds of Canadians nearing or in retirement do not understand that waiting to take their CPP benefits will increase their monthly pension payments. (Employment and Social Development Canada, 2020)

Bad advice – much of the financial planning advice focuses on the “breakeven age” which is the age you need to live till to receive more money by delaying.

This approach is misleading and doesn’t consider the largest risk for most retirees – the risk of outliving their savings (longevity risk).

Stability of CPP and OAS pensions – Canadians are concerned these pensions will not be around in the future

CPP is one of the most stable pension plans in the world. Significant changes were made in the 1990s to the structure and funding to ensure stability. The most recent report on CPP (completed by the Office of the Chief Actuary) said the pension is sustainable for at least the next 75 years.

OAS comes from general government revenues, so it is more vulnerable to cutting by the Canadian government. Yet seniors are one of the most important voting blocks in elections and reducing OAS benefits would be politically disastrous.

Fear and uncertainty – no one knows how long they will live so many opt to think in the short term and secure the money now rather than consider the long-term impact.

The greater risk to most retirees is that they outlive their savings. The average life expectancy of a 60-year-old in Canada is now 86 years old. This means retirement savings need to last 20-30 years. Delaying CPP and OAS locks in a much higher secure income, thereby reducing the chance of outliving your money.

General Recommendations

Delay the start of CPP and OAS while fully employed.

It is more beneficial to delay CPP after age 65 than OAS.

Delaying CPP – increases benefits by 0.7% per month after age 65

Delaying OAS – increases benefits by 0.6% per month after age 65

High-income seniors should seriously consider delaying OAS due to the OAS clawback.

For every dollar of taxable income above the threshold ($81,761 in 2022) you must repay $0.15 of OAS income. By delaying OAS, you can avoid the 15% OAS clawback until age 70.

Conclusion

Most Canadians in reasonable health who can afford to delay their CPP and OAS benefits should do so. The biggest risk for retirees is not having secure income for life and delaying pension benefits can help address this risk.

We encourage you to seek advice from an expert on your personal situation as the decision should be considered within the broader context of your retirement plan. Each situation is unique and deserves specific contemplation. We would be happy to help you if you have any questions or need help analysing this decision.

Citations

MacDonald, B.J., (2020). Get the Most from the Canada & Quebec Pension Plans by Delaying Benefits: The Substantial (and Unrecognized) Value of Waiting to Claim CPP/QPP Benefits. National Institute on Ageing, Ryerson University.

Employment and Social Development Canada (ESDC) (2020). Summary – ESDC Survey on Pension Deferral Awareness. Ottawa, ON: Government of Canada.

Office of the Chief Actuary. (2019). 30th Actuarial Report on the Canada Pension Plan as at 31 December 2018. Office of the Superintendent of Financial Institutions.

The third quarter saw strong markets in July replaced with negative sentiment in August and September. In the aftermath of two hurricanes striking Canada and the United States in the past two weeks, I am reminded of the headwinds that push down the prices of the valuable assets we own in our investments:

Higher interest rates. The US Federal Reserve and Bank of Canada have continued their pursuit of higher interest rates to bring inflation back under control. The Bank of Canada overnight rate is now 3% higher than it was at the start of this year. These higher interest rates, while a good thing, raise borrowing costs and can impede the growth prospects of real assets. A $1,500 monthly mortgage payment in 2020 could finance a $350,000 mortgage. Today it can support less than half. (Source: Federal Reserve Economic Data)

Recession fears. Higher interest rates have already taken a bite out of global economic growth. Lower growth can lead to lower profits and compress the value of businesses we own in our mutual fund portfolios.

Ongoing political uncertainty. As expected, the war in Ukraine lingers on. Uncertainty is the enemy of investment and prevents investors from deploying assets into businesses. Steps toward resolution will reduce uncertainty and market volatility.

Emotion Battling Our Beliefs

It is inevitable that these lower prices evoke an emotional response and may lead us to question the wisdom of our investment strategy. This is normal and to be expected – and it is (again) at times like these that we benefit by drawing on the things we know to be true and will continue to be true in the future. Here they are:

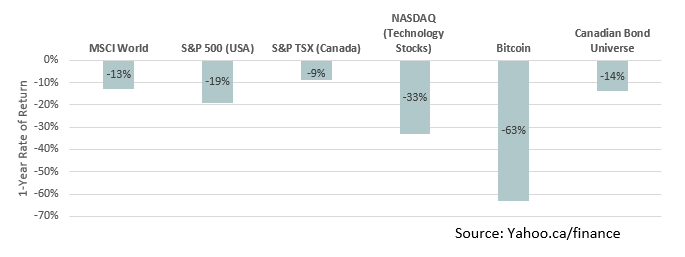

Active management can protect you on the downside. When markets are up, investors tend to prefer higher-risk investments such as a pure index ETF (S&P 500 index down 24% YTD), highly-leveraged growth stocks (NASDAQ index down 32% YTD) and/or speculative assets such as Bitcoin (down 57% YTD). We are never pleased when the value of your investments goes down in the short-term – and we are very pleased with many of our actively managed portfolios that have performed substantially better than these higher-risk investments

Our moment of greatest investment opportunity usually approaches when prices are low and uncertainty is high. This is a very difficult truth to embrace for most investors because a decision to commit to a good investment at a great time is often a lonely decision and filled with uncertainty. At the same time, a decision to remain committed to a long-term investment plan is easy when markets are up, and difficult when they are down.

We are willing to adapt your investments to a changing environment. In this regard, we have a renewed appetite to use interest-bearing investments such as savings accounts to grow your capital. We have access to the CI high interest savings account that is now yielding over 3%. If you are holding a substantial balance in your bank account, I encourage you to speak to us about this investment.

The Canada Pension Plan (CPP) and Old Age Security (OAS) form the base of Canadian retirement income. If you are entitled to the full CPP and OAS pensions you can receive roughly $23,000/year at age 65 (as of 2022). These programs are not meant to supply your full retirement income and will need to be supplemented by retirement investments or other pension plans.

What is OAS?

Old Age Security is a monthly payment out of general government revenues. You can begin collecting OAS at any time between age 65 and 70.

Eligibility

If you are living in Canada, you must:

Be 65 years old or older

Be a Canadian citizen or legal resident at time of OAS approval

Have resided in Canada for at least 10 years since the age of 18

If you are living outside Canada, you must:

Be 65 years old or older

Have been a Canadian citizen or legal resident of Canada on the day before you left Canada

Have resided in Canada for at least 20 years since the age of 18

To receive full OAS benefits you need to have lived in Canada at least 40 years after age 18.

How much can you collect?

The 2022 payment is $666.83/month (8,004/year) if you began collecting at 65 and are eligible for the full amount. If you are 75 and over, an automatic 10% increase to your OAS was enacted July 2022.

For every month you delay OAS the benefit payment increases by 0.6% (7.2%/year) up to a maximum increase of 36% at age 70. If you delay benefits till age 70 the monthly benefit is $906.89 ($10,883/year).

Guaranteed Income Supplement (GIS)

GIS is an additional tax-free monthly payment for low-income seniors. Low-income in 2022 is considered below $20,208 if single or $26,688 as a couple (not including OAS/GIS income). The amount of benefit received depends on the net income of the previous tax year. To calculate your exact eligibility refer to the Government of Canada website.

OAS pension recovery Tax (clawback)

OAS clawback refers to the repayment of OAS benefits at net income levels over $81,761 (2022). For every dollar of net income above this threshold 15 cents of OAS is repaid. OAS is fully repaid at $134,253 (under age 75) or $136,920 (age 75 and over). Effectively this is a 15% additional tax on income between these thresholds, resulting in some of the highest marginal tax rates in Canada.

What is CPP?

Canada Pension Plan (CPP) is a contributory pension plan. All employees and self-employed individuals in Canada (except Quebec, which has QPP) contribute to CPP. These individuals then receive pension income in retirement.

Contributions

Employees contribute 5.70% of employment income with the employer matching the contribution. The maximum contribution for an employee is $3,499.80 (2022) and there are no contributions on employment income over $64,900 (2022). A self-employed individual must pay both the employee and employer portions; therefore, the rate is 11.40% to a maximum of $6,999.60 in 2022.

Investment Fund

Unlike OAS, the Canada Pension Plan is an independently managed pension fund. It is separate from government revenues/expenses and is managed by an arm’s length organization, CPP Investments. The mandate of CPP Investments is “to invest the assets of the CPP Fund with a view to achieving a maximum rate of return without undue risk of loss.”

As of March 31, 2022, the fund value was $539 billion, and the fund had a rate of return of 10.8%/year over the last 10 years. The investments within the fund are wide-ranging, from Canadian farmland to publicly traded companies and private equity.

The CPP Investment Fund is subject to actuarial review every 3 years by the Office of the Chief Actuary. This is a fully independent office that reviews various pension plans and social programs, including CPP and OAS, to ensure that they are stable, secure and being managed appropriately. The most recent report on CPP was issued December 2019 where it was noted that CPP is sustainable for at least the next 75 years.

How much can you collect?

The CPP benefits you collect in retirement are determined by three main factors:

Amount contributed annually

Number of years contributions were made

Age that pension withdrawals begin

To receive maximum CPP you need to have contributed the maximum amount for 39 years between 18 and 65. You can refer to your My Service Canada Account for your CPP estimate.

The maximum monthly amount you could receive if you started your pension at 65 is $1,253.59 (2022). Meanwhile the average benefit is $727.61/month in 2022.

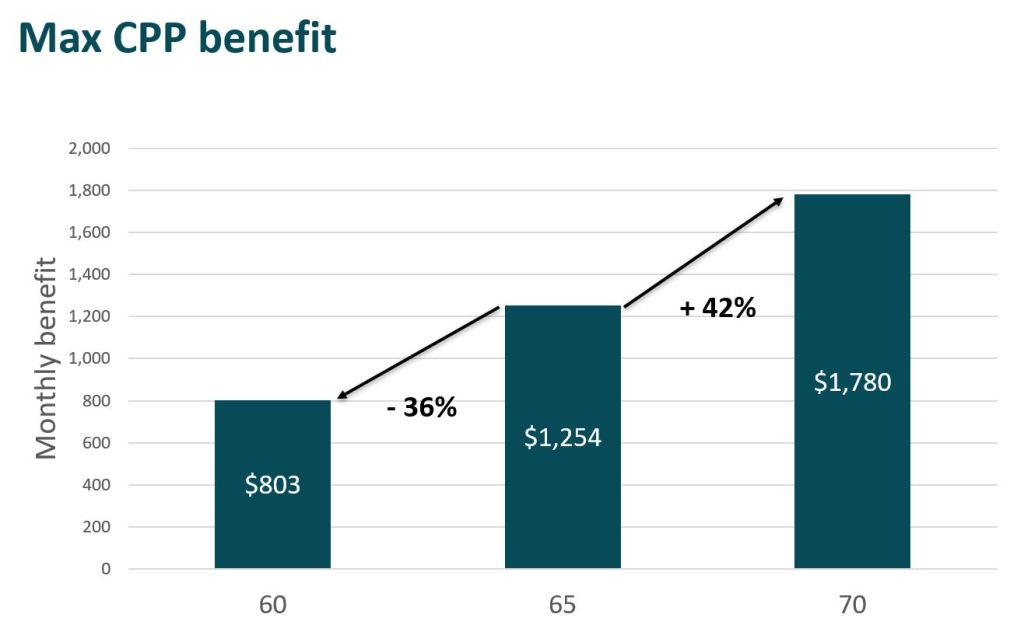

CPP benefits can be started at any time between age 60 and 70. For every month before your 65th birthday that you begin CPP benefits your pension is reduced by 0.6% (7.2%/year) for a maximum reduction of 36% if taken at age 60. Each month you delay CPP after your 65th birthday increases your pension by 0.7% (8.4%/year) for a maximum increase of 42% if started at age 70.

Therefore, if you were eligible for maximum CPP your monthly payment could be between $803 (age 60) and $1,780 (age 70) depending on when you begin withdrawing your benefits.

Refer to the CPP website for further details such as post-retirement benefit, disability pension, survivor’s pension and more.

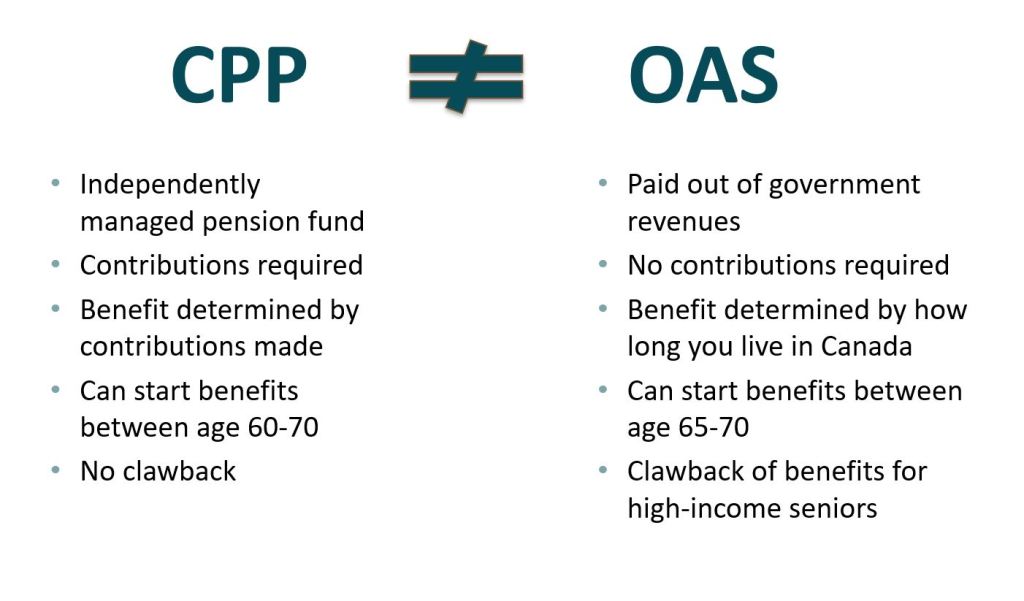

Differences

Although Canada Pension Plan and Old Age Security are pensions to support Canadian retirees, they have significant differences.

In our next post we will explore the benefits of delaying your pensions.

Higher Interest Rates, a Looming Recession and High Uncertainty

During the second quarter of 2022 asset prices contracted through persistent uncertainty concerning inflation, economic growth and political unrest.

On June 15th, 2022 the US Federal Reserve increased the interest rate charged on federal funds by 0.75% which is the largest single increase since 1994 (Source: CNBC). Interest rate hikes are expected for the next nine meetings till July 2023 (Source: CME Group). The Bank of Canada will likely follow a similar path over the next year. These interest rate increases will continue until central banks are confident that inflation is under control. What this means for borrowers is that they can reasonably expect rates on 5-year fixed mortgage to be greater than 6% at this time next year.

There are risks to our economy as these aggressive rate hikes could tip us into a recession – but slow rate hikes may allow inflation to remain. At a time like this we might be inclined to take our money and retreat to a safe place while things get sorted out. That would be a mistake and this is why it’s so important we lean on our investment discipline to guide our asset allocation decisions. This principle applies to both our behaviour and the investment approach applied by our investment partners. When we combine the discipline of these two the results are pleasing.

What helps us sleep at night

This is a question that people ask more frequently during down markets. EdgePoint Wealth recently published an article that explains in detail their investment approach and how it applies to specific investments and opportunities in their portfolios. We believe this is a worthwhile read for investors – and especially those who invest in their portfolios.

The Psychology of Money

Our team recently attended a presentation by Morgan Housel who is an author and former journalist at the Wall Street Journal. Morgan shared some of the lessons from his recent book entitled “The Psychology of Money” and I thought I would share two of them with you here:

Lesson #1: Timing is meaningless, time is everything. When Morgan published his book in 2020, Warren Buffett’s net worth was $84.5 billion. Of that, $84.2 billion (or 99.6%) was accumulated after his 50th birthday. Although Buffett has enjoyed strong investment returns over the course of his life, it has been the time he has been investing that has had the greatest impact on the compounding of his wealth. If, for example, he had begun investing at age 30 (rather than 10) and stopped investing at age 60, his investing time horizon would have only been 30 years and his net worth would have been $11.9 million. This is a powerful lesson that investing is not about each year’s individual investment returns, instead it is about having an investment plan that you can stick with and that can be repeated over a long period of time – ideally over a lifetime

Lesson #2: You can plan for every risk except for those that are too crazy to cross your mind. These “crazy” events happen more than we think and avoiding them is impossible as they cannot be anticipated. It is, therefore, important to create redundancy in our financial plans. Housel referenced suspension bridges which are built to stand even with missing cables. In the same way that a suspension bridge does not rely on a single cable, your financial life should not rely on a single investment. We incorporate different holdings and different asset classes in financial plans (equities, bonds and cash) for this very reason. These alternatives provide safety not only for risks we anticipate but also for those we cannot. The cash and low-volatility assets can be accessed when disaster strikes or deployed into the market when opportunity arises.

If there is anything we have learned the past few years, it is to expect the unexpected. From a worldwide pandemic to war in Europe to the highest inflation in decades; we have been confronted with large, unexpected events. This has driven home the importance of having a safety net to protect from these shocks.

An emergency fund is intended to protect you and your family from these shocks and help you weather financial setbacks without getting pushed off course.

It will keep you from entering debt to cover unexpected expenses or tapping into your retirement savings to cover a work absence due to a month-long accident/illness. It is also there to provide peace of mind and free you up to be more aggressive with your other investments.

An emergency fund is typically suggested to equal three-to-six months of basic living expenses. Depending on your situation it may make sense to have even nine or twelve months worth.

Figuring out your monthly spending means tracking your expenses for a few (at least three) months. If you cannot bring yourself to complete a full tracking of your spending then just average three months worth of your income (paycheque, pension, RRIF withdrawals etc.) to get a rough estimate of monthly needs.

Now you must decide how many months of expenses to cover. This depends on your personal situation and risk tolerance. Here are questions to consider:

Is your job and pay stable? If no, then the higher end of the range would be better.

Do you often worry about money? If money is a significant stressor for you, then have a larger emergency fund.

Are you a one-income household? If yes, then yet again, have a larger fund.

If retired, is most of your income from guaranteed sources (pension, CPP, OAS)? Yes, then a smaller emergency fund is reasonable.

These are just a few of the relevant considerations when determining the size of your emergency fund. Keep in mind your emergency fund shouldn’t be too large either. It is only to provide safety for financial shocks, it is not meant for long-term investing goals.

Where to Keep your Emergency Fund

The most important characteristics for the emergency fund are liquidity (easy accessibility) and safety from loss. If you can earn a small return, even better. For these reasons keeping it in a high interest savings account is ideal. In a chequing account you won’t earn any (or much) interest. Also, a locked-in product is not a good fit. An emergency fund is useless if you can’t access it when an emergency arises.

Most banks will offer a high-interest savings account and online banks tend to have the best rates. There are also mutual fund and ETF high-interest savings accounts available.

Don’t keep your emergency fund inside of your RRSP/RRIF as you will need to pay taxes when you withdraw the money. If you have TFSA room, it can be kept there, but you will eventually use your TFSA to hold long-term investments.

NexT Steps

To begin building your emergency fund, start by setting up automatic weekly, biweekly or monthly withdrawals from your chequing account that go straight into your high-interest savings account.

Once your emergency fund is fully funded move on to paying down debt or investing for other goals. Do not skip setting up an emergency fund, it is an essential step towards healthy finances and reduced financial stress.

Even if you have not heard of dollar-cost averaging there is a good chance you have used it in your investment portfolio or through an RRSP at work. It is a powerful investment strategy during the accumulation stage of your financial life.

What is Dollar-cost averaging?

It is the system of investing a fixed dollar amount at regular intervals (monthly, weekly) to purchase investments. Here is a quick example to explain:

You decide to save $500/month and set up an automatic contribution to your investments. Here are the purchases for the first three months.

Month

Contribution

Cost per unit

Number of units

January

$500.00

$50.00

10

February

$500.00

$30.00

16.67

March

$500.00

$40.00

12.50

Total

$1,500.00

39.17

After the purchase in March, you have 39.17 units and a total investment of $1,566.80 (39.17 * $40.00). Seeing the unit price decline 20% from January to March, you might assume that you lost money. In fact, you are up almost $67 or 4.45%. This is because dollar-cost averaging automatically makes you purchase more units when an investment is “on sale” and buy less when it is expensive. This is the beauty of dollar-cost averaging, it uses the volatility of investments to your advantage.

Other Benefits

A big benefit of dollar-cost averaging is the simplicity to implement, all you need is to determine the amount you can regularly contribute and then you leave it on autopilot. It also helps form the habit of regularly and automatically contributing to your investments.

Dollar-cost averaging helps to control the emotional response when volatility inevitably strikes your investments. When your investments decline in value you can know that you are taking advantage of this decline by buying more “on sale”. This reduces stress and regret through the volatility inherent in long-term investing.

Most importantly dollar-cost averaging removes the decision on when to invest because it is on aut0pilot. It is no longer necessary to spend time wondering “is now a good time to invest? Or should it wait till next week or next month?”. This automatic approach reduces the stress around the timing of contributions and stops the futile attempts to time the market.

The Other Option

Without the scheduled contributions of dollar-cost averaging you must make the decision on when to invest each contribution. This inherently leads to trying to time the market with your contribution. Using the same investment as above; here is an example of what can happen when not using dollar-cost averaging.

The first month you don’t want to put the money in as you don’t know where the market is going, so you save the $500. In the second month you don’t want to invest in something that just lost 40%, so again you wait. Now you have $1,000 in cash and no investments. In the third month you see the investment increase to $40. Now that it is moving in the right direction you invest. Good thing you didn’t buy at $50, too bad you didn’t buy at $30.

In this example you end up investing the same $1,500 but you only have 37.5 units at the end instead of 39.17 units. You also missed any dividends or interest paid out by the investments in the first two months. The worst part is that each month (or week or day) you must decide if you are going to invest or wait for the market to drop/increase. This is a mentally exhausting way to invest. It is impossible to consistently invest at the “right” time, so there will inevitably be regrets on the timing of your investment.

Conclusion

Dollar-cost averaging is a high-impact contribution strategy that is simple to implement and reduces stress and regret. It is a great fit for long-term investment goals that require regular contributions over an extended period of time (ex. retirement).

Uncertainty goes hand-in-hand with market volatility – and political uncertainty offers no exception to this rule. Think back on the summer of 2015. The S&P 500 dropped by over 12% on fears that Greece would default on its debt and exit the European Union (Grexit). In the summer of 2016 markets again dropped as Great Britain initiated its own process to exit the European Union (Brexit). Later that year in November, the S&P 500 futures dropped by over 5% on the evening Donald Trump shocked the world by winning the US presidential election (it recovered overnight and was up by over 1% the next day). The Russian invasion of Ukraine did not come as a surprise to the world. The S&P 500, nevertheless, convulsed in the first quarter – dropping by over 13% by March 8. (Source: yahoo.ca/finance).

It is during these times of market volatility that we are well-served to check our convictions on why we own what we own. This is process is known in our industry as conducting due diligence. It is defined by the Oxford Dictionary as: a comprehensive appraisal of a business undertaken by a prospective buyer, especially to establish its assets and liabilities and evaluate its commercial potential.

Due Diligence

In our investing process we employ professional managers who are constantly conducting due diligence on our behalf. They ask questions such as:

Does the business solve compelling problems for its customers – and will it continue to do so in the future?

Is the business able to generate a solid stream of free cashflow from its operations?

Are the business managers competent, honest and hard-working? Do they have a successful track record?

Is the business well-positioned to survive a crisis?

I encourage you to ask the same questions too. If for no other reason than to reassure yourself that you are holding shares in businesses that will provide for you and your family in the future. If you have a moment, look up the securities you hold in your mutual fund portfolios and ask yourself if these are the kinds of businesses you want to own in a volatile world. Search for the top holdings of your mutual funds (this information is publicly disclosed and updated each month).

Canada’s inflation rate is the highest it has been since 2003. Last year we experienced a 4.7% increase in the Consumer Price Index (CPI) (StatsCan: reported November 2021). Annual inflation in the US is running at 6.8%, Germany 5.2% and the UK 4.6% (Source: OECD). This is much higher than many of us have experienced in over 20 years and those under the age of 40 may have never experienced in their lives.

Inflation is in the news with good reason – because we see and feel price increases when we shop too. We want to be a part of the discussion and navigate it together with you.

WHat is Inflation?

Inflation is the decline of purchasing power of your money over time. It is often measured by comparing the price of a basket of goods and services from one year to the next. If the basket cost $100 in the first year and $102 in the second, then inflation would be calculated at 2%. This basket of goods and services method is a useful tool to measure inflation. Yet it is only measures inflation of the goods and services included in the basket in the proportion they determine. Alcohol, tobacco and recreational cannabis, for example, feature prominently in this basket. If your spending on goods and services differs from the CPI proportion, you may experience higher or lower prices than the CPI would indicate. Click here to see what is included in the CPI basket.

A one-year increase may seem inconsequential but over decades this can really add up.

Hyperinflation

The most extreme examples of inflation are those in countries such as Zimbabwe in 2007 – 2009 and Germany between World War I and World War II. In these countries inflation was so high that the prices of goods were doubling every few days. This led to wheelbarrows of cash being used to buy groceries, or cash being burned because it was cheaper than using it to buy wood. These are extreme outliers often driven by unique and specific circumstances such as civil unrest and war (Source: Forbes). We have here in our office a $50 trillion bill (its current value is ~$20, but only as a collector’s item) from Zimbabwe that serves as our reminder of what “money” means. It is simply a claim against real goods and services. If more money is injected into an economy with no more goods and services to consume with that money, then it stands to reason that more dollars are competing for the same things and prices must increase. This is a truth learned the hard way in countries such as Zimbabwe where the value of a dollar became effectively worthless.

WHat causes Inflation?

The causes of inflation are both simple and complicated.

The simple reason for inflation is a mismatch between demand and supply. This is because either there is additional demand or a reduction in supply that forces the price up. In a healthy economy this inflation is mitigated, businesses can increase production to meet the demand and most supply disruptions are temporary in nature or can be worked around.

During the pandemic we have experienced both. Many service businesses closed, resulting in individuals having more money available to purchase goods. At the same time disruptions in production and shipping resulted in lower supply. This combined to increase the costs of many goods and services.

The more complicated causes of inflation are driven by fiscal and monetary policy. Stimulative fiscal policy moves by the government such as cutting taxes or spending on infrastructure projects lead to increased demand for goods and services leading to inflation. The monetary policy decision to reduce interest rates leads to more money being available to be lent to business and consumers. This increases the money available throughout the economy to be spent on goods and services, increasing the costs.

Those in charge of fiscal and monetary policy have a tight rope to walk as they navigate keeping the economy growing while at the same time keeping inflation low.

Over the past two years extraordinary amounts of money has been added to economies and interest rates at historically low levels were dropped even further to mitigate the financial effects of the pandemic.

Finally, inflation is also driven by sentiment. If businesses believe their costs will increase in the future, they will increase their sale prices. If individuals believe the price of goods will increase, they will demand higher wages which increases costs for their employers which leads to increased sale prices. As you can see the fear with inflation is that it feeds on itself and becomes self-reinforcing.

What Are the predictions?

Economists are about as good at making accurate predictions as meteorologists, but many of them see this increase in inflation being temporary. As we move past the pandemic and supply chains are repaired, many economists see inflation settling back to the 2-3% range by the end of 2023 (Source: OECD).

To achieve this goal of decreasing inflation, central banks across the developed world will begin increasing interest rates, likely multiple times in 2022 and 2023. This reduces the availability of money in the economy and should result in a dampening of inflation.

What Can We Do?

The first advice is not to panic. It is unlikely we will see inflation anything like the double-digit inflation of the 1970s. Inflation is higher than we are used to and is likely to stay higher for the next two years. This does not forebode a new world where drastic action is necessary.

As mentioned earlier, inflation is the decline of purchasing power of a currency. Therefore, those who are most affected are those who are holding large amounts of cash or assets denominated in currency, such as bonds. These assets become less valuable in a high inflation world.

We believe that the best place to invest your money over the long term is into the ownership of a diversified basket of quality businesses through the mutual funds you own. These are businesses that can increase prices to maintain their profit margins and have the flexibility and ability to adjust to changing business conditions. This approach is what has enabled our clients to succeed in a variety of economic environments over 50 years – and why we are committed to continuing with this discipline.